OTTAWA, ONTARIO

Market Update - Summer 2025

Are you looking to buy or sell a home in Ottawa? Are you hearing conflicting information on whether it’s a good time or not such a good time to buy or sell? Well, don’t go anywhere. I’m here to help you understand what is going on in Ottawa’s Real Estate market specifically so that you’ll be better prepared to decide whether it’s the right time for you to buy or sell. Make sure to stick around to the end if you’re a Seller considering selling in the next year. I have a hot tip for you that you don’t want to miss!

This update is going to cover the three summer months of 2025 and is specifically for the City of Ottawa boundaries, so it’s not the same as what you see from most of the other Realtors in the Ottawa market, as their stats cover areas outside of the City boundaries.

In preparing this update, I realized that a seasonal update like this works well for the slower seasons in Real Estate. The summer is typically a slower paced market, and this year was no exception. I’ll share with you the trends of what we saw over the June/July/August timeframe in Ottawa as we head into the Autumn season.

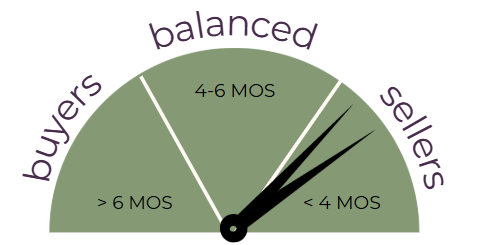

1. Months of Inventory

The first thing I’ll talk about is Months of Inventory. You might wonder what this is, and why is it important? The months of inventory is a measure, or ratio, of how many homes are on the market and how many homes have sold in a given month. It represents how many months it would take to sell all of the currently listed homes, given the current rate of home sales, if no more homes were listed for sale. The key here is that it is affected by not only how many homes are on the market, but also how many homes are selling. Both of these change throughout the year, creating an always shifting value of Months of Inventory. The trend of MOI is what is important.

As a Buyer, you want to see higher MOI, meaning more selection of homes and fewer buyers. As a Seller, you want a low MOI, meaning more competition, which can mean quicker sales and potentially upward pressure on prices.

Months of Inventory changes with the seasons. The highest MOI is typically in December and January when there simply aren’t many buyers out shopping. The lowest MOI typically is seen in May when most buyers are out shopping, and that is what we see for this summer update – the MOI rose throughout the summer month, from 2.8 months in June up to 3.7 months in August, due to sales slowing down through the summer months while inventory levels remained quite high.

And, compared to last year, the MOI is up just the slightest bit.

When we break it down into the three main property categories, we can see that the market is not the same for all property types. If you’re looking at a detached home, the MOI rose from a little shy of 2.5 months in June up to 3.5 months of inventory by August.

The months of inventory for freehold Townhomes didn’t change much over the summer, only shifting from 2.1 months to 2.16 months. This confirms that the market for townhomes remains much quicker than the other property types.

And finally, the months of inventory for Condominium apartments has increased from 3.62 months in June up to 4.44 months of inventory in August. This is squarely in a balanced market, where negotiations for pricing, conditions, and closing dates are more common.

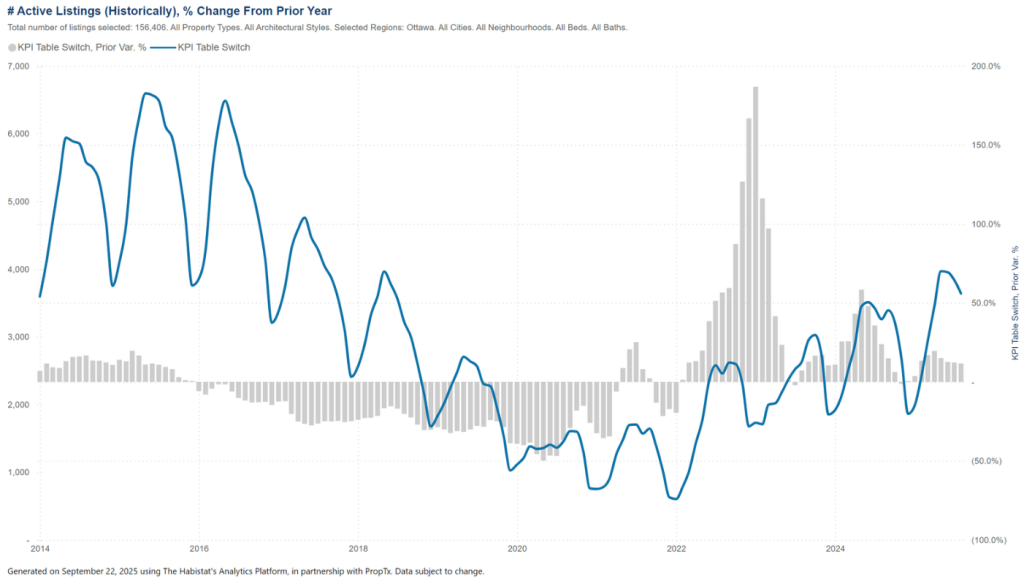

2. Inventory Levels

As I mentioned, Months of Inventory is calculated based on the sales as compared to the Inventory levels. This chart shows us the level of Inventory for the City of Ottawa, the blue line, over the past number of years. It is clear that the levels of inventory have been climbing since 2022, and you can also see how the inventory levels are cyclical throughout the year.

The gray bar chart superimposed on this chart shows you the change of inventory year over year for any given month. You can see periods where inventory levels were dropping for years, notably 2016 through 2021. And you can also see periods of inventory climbing, such as 2014 through 2016 and now 2022 through 2025.

I’d like to point out that the trend of increasing inventory appears to be slowing, which may result in the inventory leveling out in the next year or so. If sales continue to be higher in the months and years to come, we may have found a new balance within the market. What we don’t want to see is a drop in inventory back to the levels seen in 2019-2022, which came with unsustainable price increases.

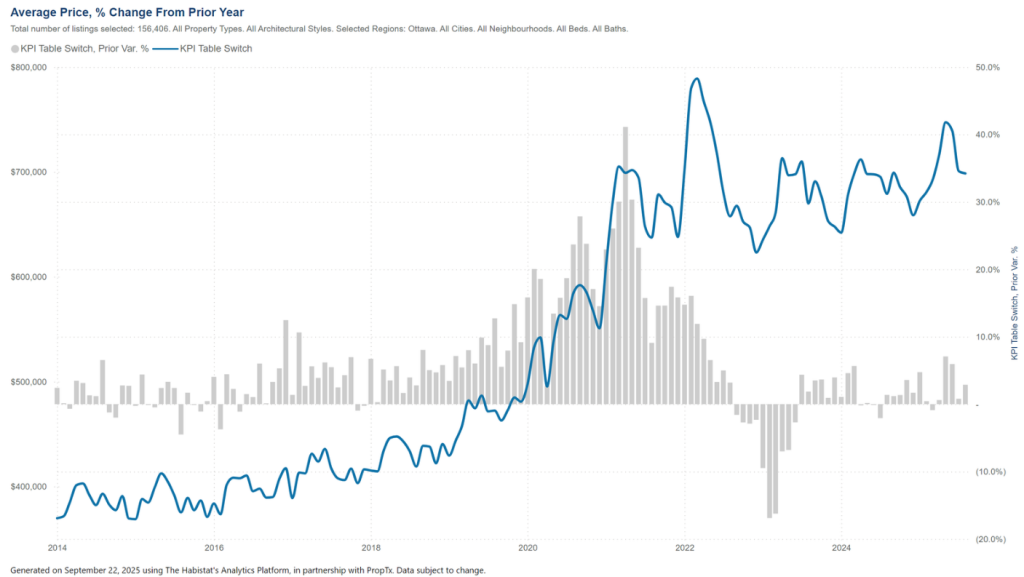

3. Average Sales Price

Next, let’s talk prices. The average sale price of all properties across the City of Ottawa in this summer was $739k in June, $701k in July, and $700k in August. This was a steady downward trend from $741k in May. This downward trend of average prices is completely normal, as peak prices typically are in late spring each year. The second column shows that the average prices for the summer months are all above the prices we saw those same months in 2024.

This chart shows you the average sale price across Ottawa since 2014, represented by the blue line, as well as the year over year change for each month, represented by the grey bars. You can see that over the past 13 months, there has only been one month where the average sale price was below the year prior, but the price gains have been quite low.

If you can think back to the similar chart I showed with the inventory, you’ll see that the price gains on this chart correspond to the same period of time where the inventory levels were extremely low.

On this chart, you see that between 2014 and about 2017 the prices weren’t changing too much beyond the seasonal ups and downs. It was only in 2017, about a year after the inventory levels started to drop off (from the other chart), that the prices started to go up significantly.

My feeling is that slow and steady, like that period in 2014 through 2017 and now from 2022 till now is a lot better for both buyers and sellers for the long run. Real Estate shouldn’t be a speculative sport.

4. Days on Market

The next thing we’ll look at is how long it’s taking for homes to sell. This is the Days on Market, and represents the time on market for those homes that have sold. City wide, we saw an average of 30 Days in June, 34 Days in July, and 38 Days in August. Note that it is completely normal for the summer months to have higher days on market, due to lower sales volume. Comparing the Days on Market to last summer, we see that this summer was a bit slower, by between 1-3 days.

Breaking it down into property types, we see detached homes took an average of 27 days to sell in June and 30 days in July, and 34 in August, which is a mix of slightly slower and quicker than in 2024. For freehold townhomes, we saw an average of 26 days in June, 28 in July, and 35 in August, which is a little bit longer than 2024, which ranged from 22 to 31 days. And, finally, for condo apartments, the average days to sell this summer was 46 days in June and July, and 50 days in August, as compared to 33-45 days in the summer of 2024. The condo market has definitely been the slowest market this year, which may be affected by all of the headlines coming out of Toronto on their exceptionally slow, almost dead, condo market.

5. List to Sale Price Ratio

The final metric of how the market is doing that I’ll share is the Average list-to-sale ratio. It is a measure of how close the asking and selling prices are. This summer, we saw the List to Sale Ratio drop from 98.5% to 98%. Year over year, this was also down, by 0.1 to 0.3%. This drop stems mostly from the higher inventory levels and higher Months of Inventory we are seeing this year.

6. Intrest Rates

If you’re looking to buy in the near future or need to renew a mortgage that you currently have, there is good news in that the overall trend of mortgage rates has decreased over the summer.

The Bank of Canada just dropped their overnight lending rate by 0.25% in mid-September, which was the first drop since March 2025. The overnight lending rate affects the Bank Prime rates, and thus the Variable rate mortgage options. The fixed rates are set by banks based on the 5-year bond rates, which fluctuate more often.

Right now, the variable and fixed rates offered by banks in Canada are both at around, or slightly below 4%.

As always, it is absolutely essential that you talk with a mortgage broker, ideally, or your representative at your bank to find out what the rates are for you and your specific situation. I know a little about mortgages, but they are the experts!